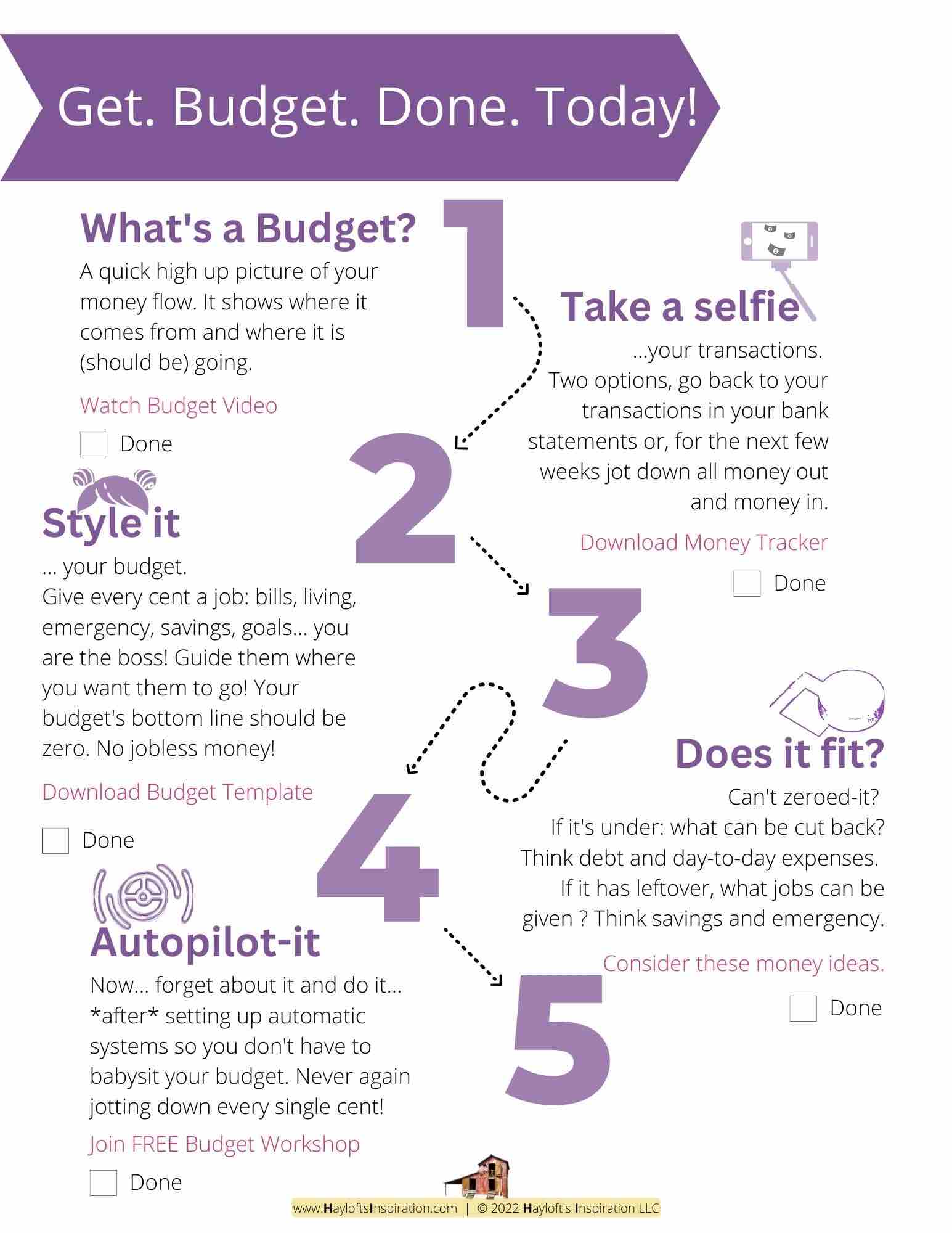

Start Early, Reap the Rewards

.

.

Hola!

Retirement might seem like a distant goal, something you’ll worry about “later.” But believe me, when it comes to securing your financial future, “later” comes a lot faster than you think.

Whether you’re just starting your career or are mid-way through it, there’s no better time to start planning for retirement than right now. Trust me—your future self will thank you.

Let’s dive into seven essential tips to get you on the right track and ensure you’re setting yourself up for a comfortable, worry-free retirement.

.

1. Start Contributing to a Retirement Account Early

The sooner you start contributing to a retirement account, the better. This is all about the magic of compound interest. It’s like planting a tree—the earlier you plant it, the bigger and stronger it will grow over time.

Imagine this:

if you start putting away even a small amount in your 20s, your money has decades to grow. Let’s say you invest $100 a month starting at age 25 with an average annual return of 7%. By the time you’re 65, that money could grow to over $260,000. Now, if you wait until you’re 35 to start, even if you contribute the same amount, your savings will only grow to about $120,000. That’s a huge difference!

Think about it like this: have you ever had a garden?

When you plant seeds early in the season and nurture them, they have a longer time to grow, flourish, and produce a bountiful harvest. Waiting too long means you might miss out on the best growing season. It’s the same with your retirement savings—start early, and give your money the time it needs to flourish.

.

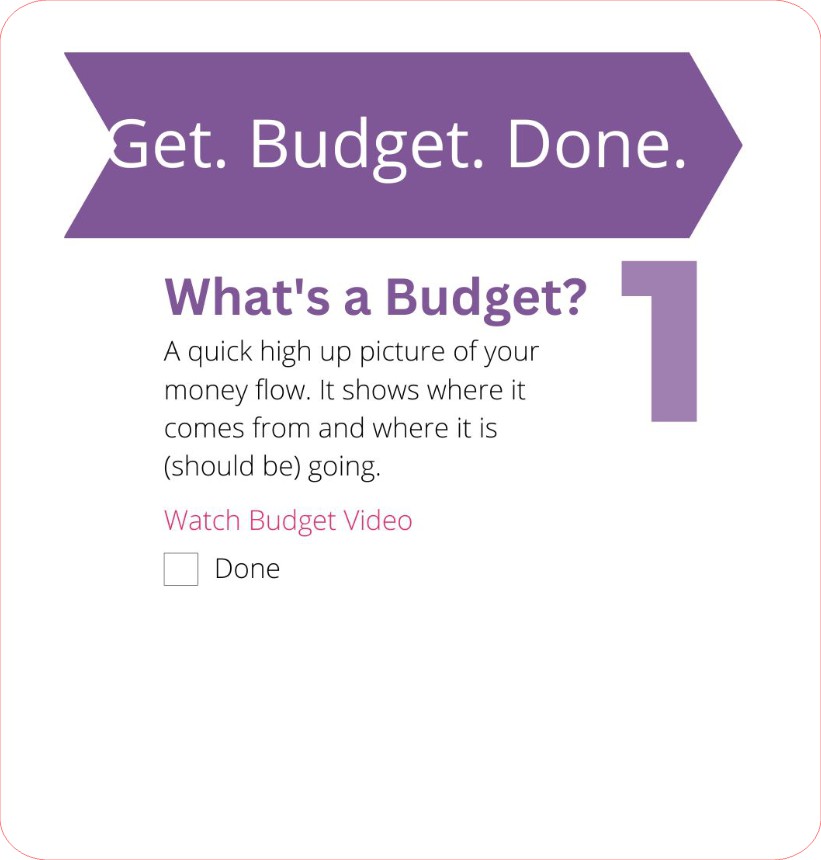

2. Maximize Employer Contributions

If your employer offers a retirement plan with matching contributions, you should absolutely take advantage of it. It’s essentially free money.

For example,

.

if your employer matches 50% of your contributions up to 6% of your salary, you’re getting an instant 50% return on that portion of your contributions. Who wouldn’t want that?

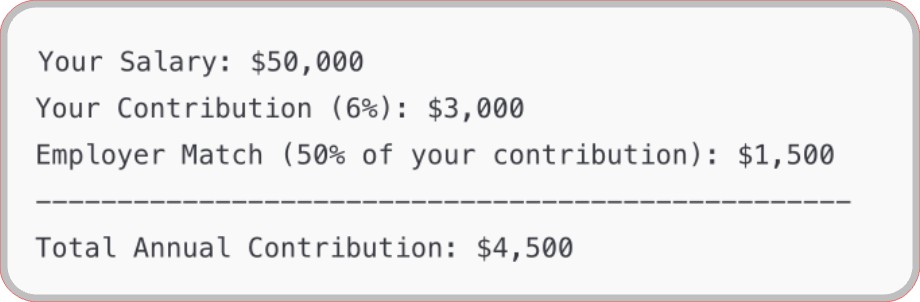

Let’s break this down:

- Your Contribution to your retirement account:

- 6% of your salary $50,000 = $3,000 per year.

- Employer Match:

- Your employer matches 50% of your contribution.

- 50% of $3,000 your contributed = $1,500 per year.

- Total Annual Contribution to Your Retirement Account:

- $3,000 (your contribution) + $1,500 (employer match) = $4,500 per year.

.

That’s an extra $1,500 added to your retirement savings each year, essentially free money from your employer. Over time, with compound interest, that employer matched amount annually, can significantly boost your retirement savings.

Think of it like this: have you ever found a coupon for something you were going to buy anyway? It’s a no-brainer to use it, right? The savings are there for the taking, just like those employer contributions.

.

.

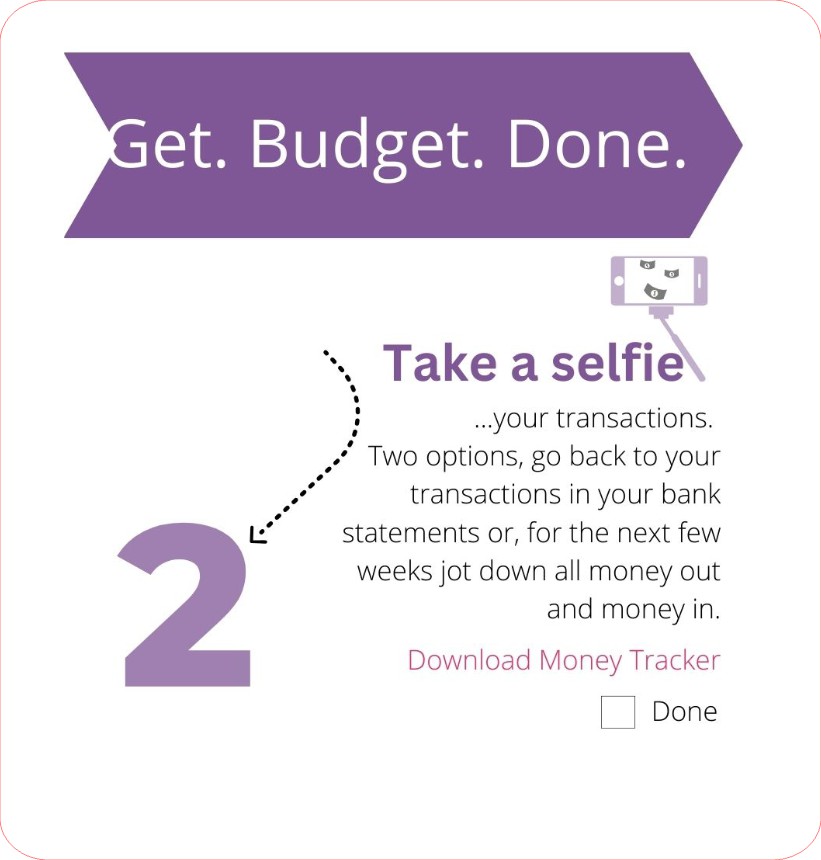

3. Diversify Your Investments

Putting all your eggs in one basket is never a good idea, especially when it comes to investing. Diversification helps you manage risk by spreading your investments across different asset classes like stocks, bonds, and real estate. This way, if one investment performs poorly, others may perform better, balancing out your overall portfolio.

For example, during an economic downturn, stock prices might fall, but bonds often perform better in such conditions. By having both in your portfolio, you protect yourself from significant losses.

Here’s a parallel:

remember when you tried cooking a new recipe and decided to “wing it” without following the instructions? Maybe it turned out great, but it was risky. If it had gone wrong, dinner might have been a disaster.

Diversifying your investments is like following the recipe—it’s a safer bet to ensure your financial meal turns out well.

.

4. Increase Contributions Gradually

As your income grows, it’s a good idea to gradually increase the amount you contribute to your retirement account. You might start small, but as you get raises or pay off debts, redirect some of that extra money into your retirement fund.

For instance, if you start by contributing 5% of your salary, try bumping it up to 6% next year, then 7%, and so on. Even small increases can have a substantial impact over time.

It’s similar to starting a new workout routine. You might begin with lighter weights or shorter distances, but as you build strength and endurance, you gradually increase the intensity. Before you know it, you’re lifting more, running farther, and feeling great—just like your retirement savings will grow stronger over time with those gradual increases.

.

.

5. Avoid Early Withdrawals

It can be tempting to dip into your retirement savings when an emergency or unexpected expense comes up, but doing so can have significant penalties. Not only will you likely have to pay taxes on the withdrawal, but you could also face an early withdrawal penalty of up to 10%. Plus, you’re losing out on future growth.

Think of it this way:

have you ever been on a road trip and been tempted to take a shortcut, only to realize it ended up taking longer and being more frustrating? Early withdrawals are like that shortcut—what seems like a quick fix can cost you more in the long run.

.

6. Plan for Healthcare Costs

Healthcare costs are one of the biggest expenses in retirement, so it’s crucial to factor them into your planning. According to Fidelity, a 65-year-old couple retiring today could need around $300,000 to cover healthcare expenses throughout retirement. That’s a staggering amount, and it’s better to be prepared than caught off guard.

Consider options like Health Savings Accounts (HSAs), which offer tax advantages and can be used for medical expenses in retirement. It’s like having a special savings account just for your health needs.

Imagine planning a vacation—if you know a particular destination is pricey, you’ll save up more to enjoy it without stress. The same principle applies here: knowing healthcare costs can be high, you can plan and save accordingly, ensuring your retirement remains enjoyable and worry-free.

.

7. Review and Adjust Your Plan

Life changes, and so should your retirement plan. Regularly review your investments, contributions, and goals to ensure you’re on track. Maybe you got a promotion, your expenses have changed, or the market has shifted—these are all good reasons to reassess your plan.

Set a reminder to review your retirement plan annually. This could be at the start of the year or around your birthday. Make adjustments as necessary, like increasing your contributions or rebalancing your investments.

Think about how you regularly check in on your health or fitness goals. You might adjust your diet or exercise routine as needed to stay on track. The same goes for your financial health—consistent check-ins ensure you’re making progress and staying on the right path.

.

.

In summary…

Start planning for your retirement today, even if it’s just setting up an account. Every small step you take now can lead to a more comfortable and secure future.

.

Your takeaway…

Life goes so fast… we know. But, are you prepared for that fast approaching future?

.

Now your turn. Share in the comments…

Do you want to have a retirement plan? If you have a plan different than the one broken down here, I’m very interested to know. I appreciate creativity!

.

.

.

.

+ View comments

+ Leave a comment